It is currently that taxpayers receive their notices of taxes and social security contributions relating to the year 2021. Many people very often find it difficult to understand this document.

Also, we publish below, a fictitious tax notice that we have cut into several numbered frames. Each of the paragraphs below has a number corresponding to a frame of the tax notice and provides an explanation of the information contained in this frame.

Obviously, we cannot give the meaning of all the information contained in this document, but you can contact us for more precise information.

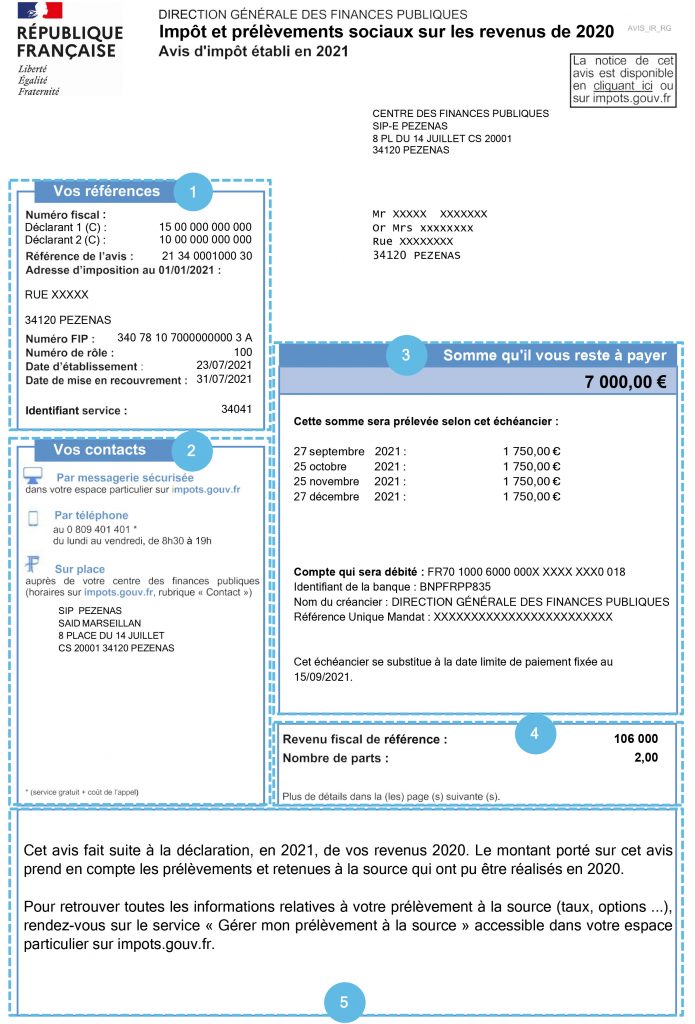

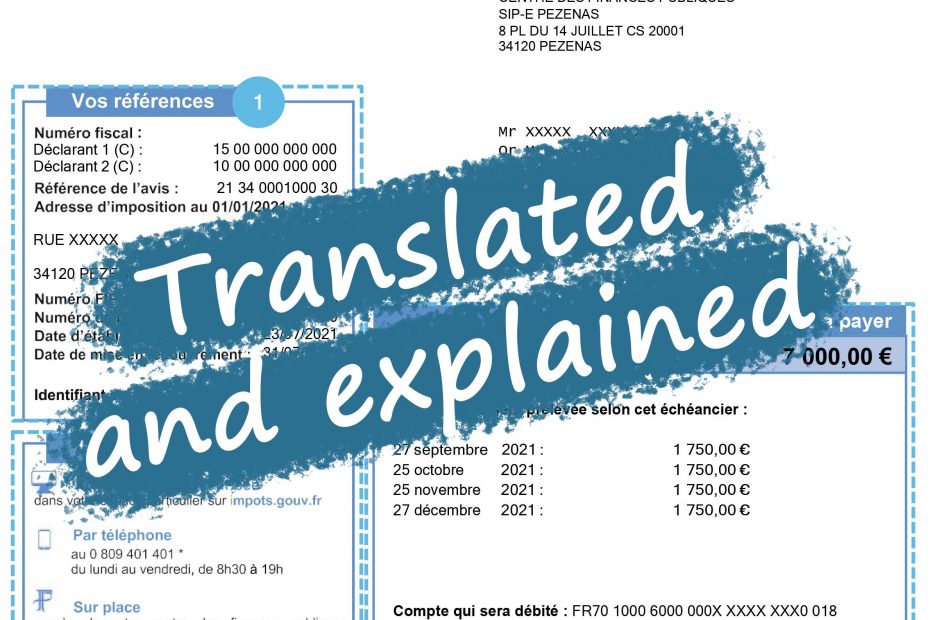

1 – “Vos références” (Your references)

This frame includes a set of identification numbers as well as your tax address at the beginning of the year, which is in principle your domicile.

The main identification references are:

- The tax number of each member declaring income within the tax household;

- The FIP number, the last two characters of which change each year;

- The tax notice number;

- The dates of issuance of the notice and collection of the tax. Please note, the date of collection is not necessarily the date on which the tax must be paid, this date appears in another frame.

2 – “Vos contacts” (Your contacts)

This paragraph does not require any particular comment, the information contained therein will be useful to you in the event of problems to be resolved with the tax authorities.

3 – “Somme qu’il vous reste à payer” (Sum remaining payable)

This is the difference between the total taxes and social contributions due for the year 2020 (and calculated below) and the total amounts withdrawn at source as well as from your bank accounts during this same year.

This balance must be withdrawn from your account according to the deadlines indicated.

In the event that the sums withdrawn during the year were greater than the total tax due, the balance is automatically refunded by the tax services.

The references of the account from which the balance will be withdrawn are then indicated and then the following sentence is noted at the bottom of the box:

“This schedule replaces the payment deadline set on September 15th 2021”.

4 – “Revenu fiscal de référence” (Reference tax income)

The reference tax income represents the total of net taxable income, income and capital gains taxed at a flat rate, income from movable capital subject to withholding tax and certain exempt income.

This amount is often requested from the taxpayer, it is used to determine the right to exemptions or reductions in taxes and duties (housing tax for example). It is also used as a reference for access to the LEP (popular savings account), for the CSG rate for retirees, for the allocation of low-cost housing or even holiday vouchers, etc.

We then find inscribed the “Nombre de parts”: this figure is determined according to the number of people making up the tax household (2 for example for a couple or 2.5 for a couple with a child). It determines how the tax is calculated, the higher its amount, the more tax will be calculated between with a low rate.

5 – The translation of the terms appearing in this box is as follows

“This notice follows the declaration, in 2021, of your income for 2020. The amount shown on this notice takes into account the deductions and withholdings at source that may have been carried out in 2020.

To find all the information relating to your withholding tax (rates, options, etc.), go to the gérer mon prélèvement à la source service accessible in your private area on impots.gouv.fr”.

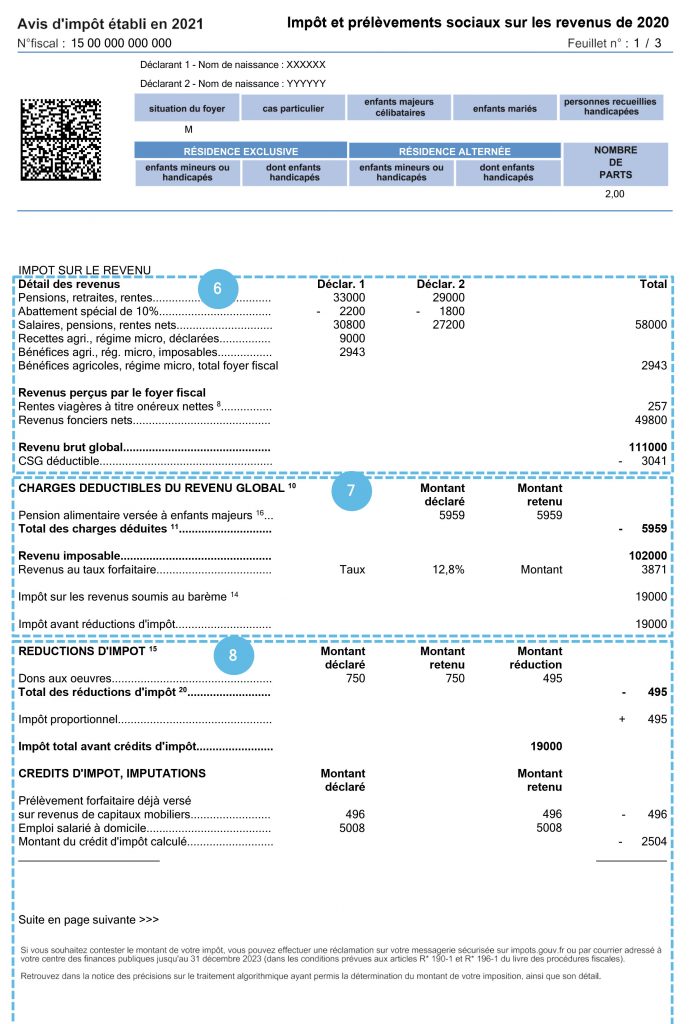

6 – “Impôt sur le revenu” (Income tax)

“Détail des revenus” (Income details): all categorical income declared by each member of the tax household subject to progressive tax are indicated on this part. These are wages, pensions, farm income, industrial and commercial profits, non-commercial profits.

Salaries and pensions benefit from a special reduction of 10% capped which is deducted from the gross base and indicated below the income concerned.

- “Revenus perçus par le foyer fiscal” (Income received by the tax household): here are indicated all other income subject to the progressive tax rate made by all members of the tax household. This mainly concerns income from property and income from movable capital.

- “Revenu brut global” (Total gross income): this is the total of all taxable income after any allowance.

- “CSG déductible”: amount of the deductible part of Social Contribution paid the previous year. This amount is deducted from the overall gross income.

7 – “Charges déductibles du revenu global” (Expenses deductible from total income)

This chapter includes all charges deductible from overall income, these charges are mainly:

- Alimonies;

- Some savings for retirement.

The following line indicates the amount of taxable income after deduction of these various charges.

Below is the total amount of income subject to a flat rate and, under the latter amount, the total income tax due at progressive rate before the various tax reductions and credits.

8 – “Réductions d’impôts Crédits d’impôts” (Tax reductions and tax credits)

- Tax reductions: here is the amount of all the expenses declared by the taxpayer which lead to a tax reduction, the main ones being:

- Donations made to certain organizations;

- Expenses for dependent children continuing their studies;

- Certain rental investments.

The figure on the right corresponds to the total of the tax reduction.

We find, next line, the amount of tax (to be added) corresponding to income subject to a flat rate (which we have seen above in box 7).

The next line shows the total tax amount before tax credits.

- Tax credits: we have here the expenses eligible for tax credit declared by the taxpayer and the amount of the corresponding tax credit. These expenses are mainly:

- Expenses for home jobs;

- Childcare costs for children under 6;

- Certain works done in the main house.

The last line of the box shows the total income tax due after all tax reductions and credits.

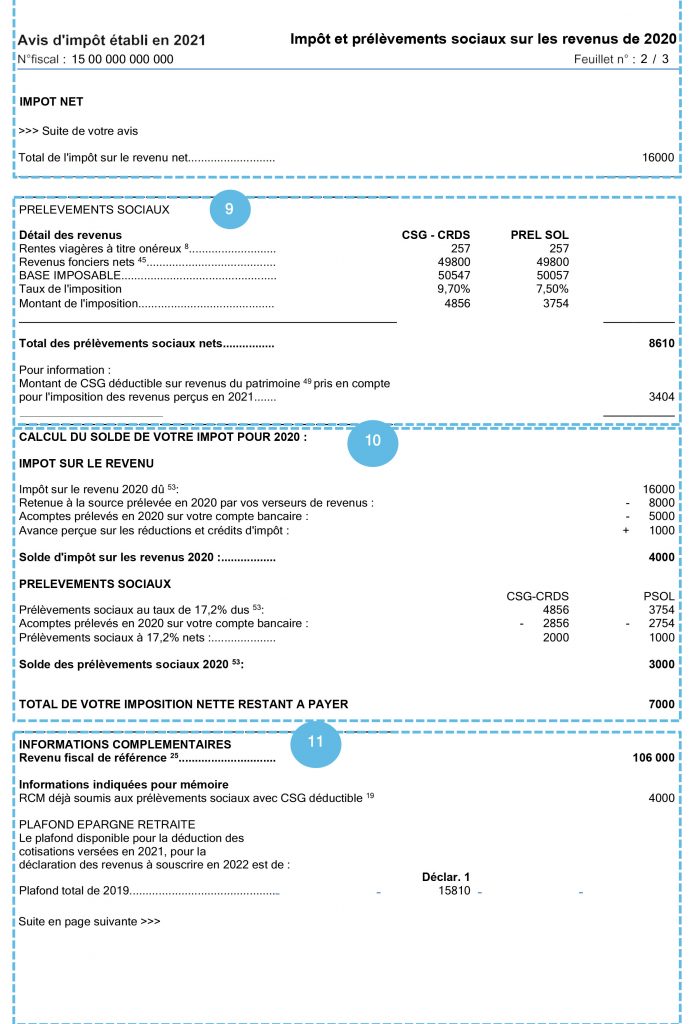

9 – “Prélèvements sociaux” (Social contributions)

This chapter shows the amount of various income that was not subject to social security contributions during the year, it is mainly:

- Certain life annuities;

- Land income;

- Certain professional income or capital gains which, for various reasons, have not been subject to compulsory social contributions.

We can see the calculation of the amount of the deductions and below on the right, the total of the net social contributions which will be added to the net tax payable.

The last line of this framework shows the share of social contributions deductible from gross income for the following year. This amount will be automatically deducted by the tax authorities, and it appears, as we have seen, at the bottom of box 6.

10 – “Calcul du solde de votre impôt” (Calculation of your tax balance)

- Income tax: are deducted from the net amount calculated above:

- Withholding tax levied during the year by income earners;

- Deposits withdrawn during the year from the bank account;

- Advance received on tax reductions and credits.

The difference represents the balance of tax outstanding or excess payments.

- Social contributions: deposits withdrawn during the year from the bank account are deducted from the net amount above.

The difference represents the outstanding balance or overpayment.

The last line indicates the total of tax and social security contributions remaining to be paid (or the possible excess of payments). We find this amount in box 3.

11 – “Informations complémentaires” (Further information)

The first line recalls the amount of reference tax income that we have already commented on in box 4.

Just below is indicated, for the record, the total income from movable capital which during the year was subject to social contributions with deductible CSG.

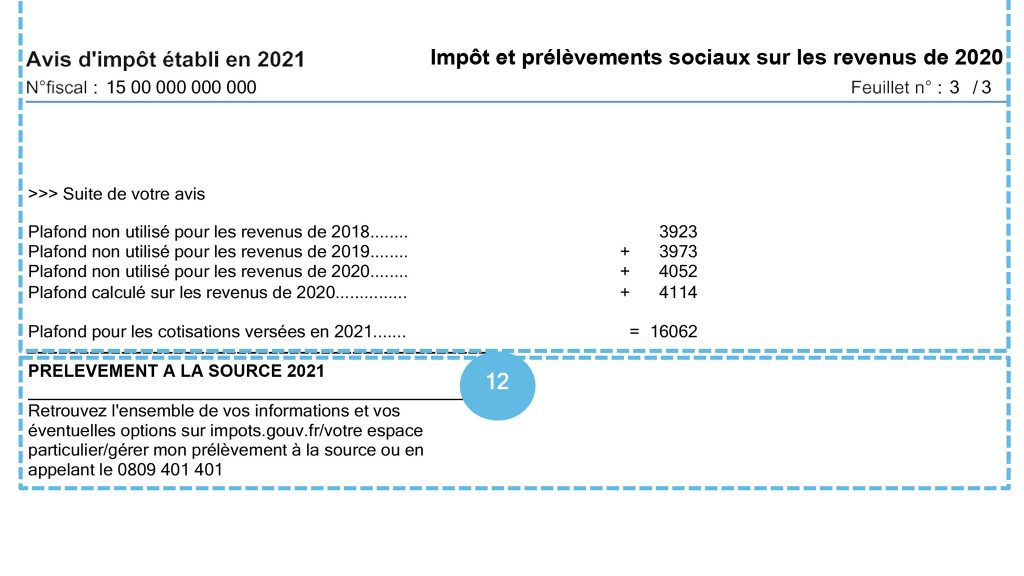

The rest of the framework concerns people who invest in one or more deductible retirement savings plans. The information given makes it possible to know the difference between the amounts paid and the deductibility ceiling over the last three years and thus to calculate the deductible ceiling for the following year.

12 – “Prélèvement à la source 2021” (2021 source withdrawal)

We translate below the terms of this framework which does not require any particular comment:

“Find all of your information and your possible options on impots.gouv.fr / votre espace particulier / gérer mon prélèvement à la source or by calling 0809 401 401”.

You now have all the information you need to complete your tax return correctly. However, if you have any doubts, please do not hesitate to contact us!